According to IMARC Group's report titled "Dairy Industry in India Size, Share, Trends and Forecast by Product and Region, 2026-2034", The report offers a comprehensive analysis of the industry, including industry growth, trends, share, and regional insights.

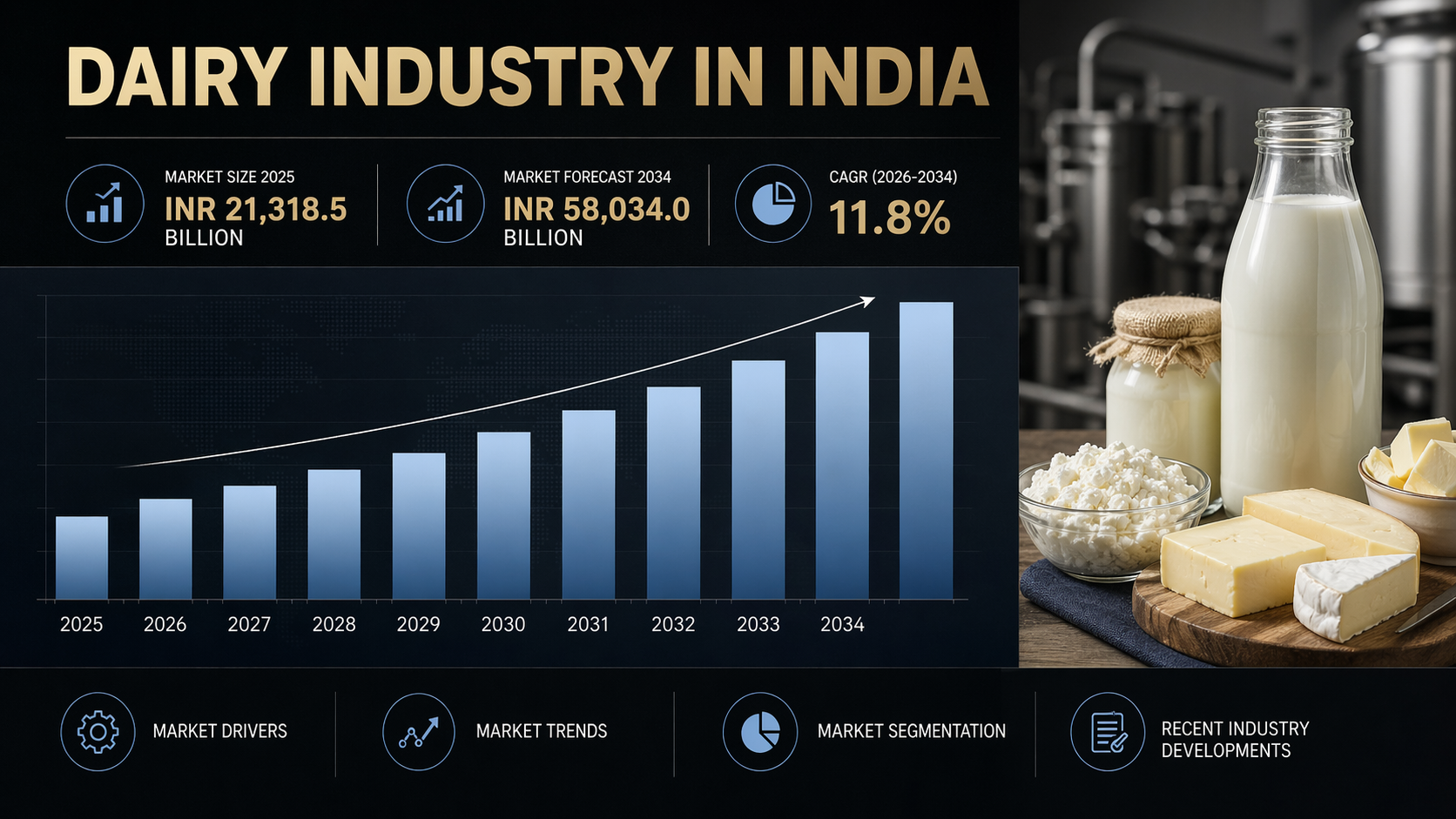

The dairy industry in India was valued at INR 21,318.5 Billion in 2025 and is projected to reach INR 58,034.0 Billion by 2034, registering a robust CAGR of 11.8% during 2026-2034.

Driven by an exponential rise in premiumization and aggressive cooperative modernization, the Dairy Industry In India: A Staggering ₹58 Trillion Boom Driven by A2 and Organics signals a lucrative transformation in agricultural processing. B2B investors and supply chain leaders are now capitalizing on an unprecedented surge in value-added formats, shifting the ecosystem from a traditional commodity market into a tech-enabled consumer packaged goods powerhouse.

- Exponential Valuation Trajectory: The Indian dairy market achieved a commanding valuation of INR 21,318.5 billion in 2025 and is projected to scale massively to an astonishing INR 58,034.0 billion by 2034, registering a robust compound annual growth rate (CAGR) of 11.8% during the forecast period.

- Global Output Supremacy: Solidifying its position as the undisputed global heavyweight, India currently generates over 248 million metric tons of milk annually, accounting for approximately 23% of total global milk production, ensuring unparalleled, long-term supply resilience for commercial processing facilities.

- Liquid Milk Dominance: While value-added segments are experiencing rapid consumer adoption, traditional liquid milk remains the structural bedrock of the industry, commanding an overwhelming 65.30% product share in 2025, heavily sustained by ingrained daily dietary reliance across both urban and rural demographics.

- Regional Procurement Concentration: Production and procurement networks are heavily concentrated in critical agricultural states, with Uttar Pradesh capturing a leading 18.70% regional market share, supported by the nation's largest bovine population and a deeply entrenched, highly organized cooperative infrastructure framework.

- Value-Added Capital Expansion: Evolving consumer palettes are fundamentally restructuring the revenue mix, driving massive capital inflows toward higher-margin, value-added products (VAP) such as probiotic beverages, organic cheese, Greek yogurt, and premium A2 cow milk tailored for health-conscious urban populations.

➤ Request Sample Report - Evaluate Core Statistics Driving Your Industry Trends

India's Strategic Vision for the Dairy Industry:

- Executing Massive Cooperative Modernization: The macro-economic vision focuses aggressively on modernizing massive cooperative supply chains, transitioning an expansive network of over 190,000 village-level cooperative societies into highly efficient, standardized commercial procurement hubs. This structural upgrade is actively spearheaded by the National Dairy Development Board to dramatically stabilize baseline farmer incomes and secure institutional supply consistency.

- Elevating Indigenous Bovine Genetics: Driven by the revised Rashtriya Gokul Mission, backed by a monumental INR 3,400 Crore allocation as of March 2025, the state is strategically elevating indigenous bovine genetics. This proactive policy directly aims to exponentially increase per-animal milk yields, building robust domestic self-reliance while heavily buffering commercial processors against seasonal supply volatility.

- Securing Global Export Dominance: By leveraging unmatched raw material volume capabilities and highly competitive localized production costs, India is strategically positioning itself as a dominant net-exporter of high-value commodities, specifically Skimmed Milk Powder (SMP) and industrial butter. The government is actively aligning local quality testing frameworks with stringent global trade compliances to permanently unlock lucrative Southeast Asian and Middle Eastern export corridors.

- Subsidizing National Cold-Chain Infrastructure: Addressing severe historical cold-chain bottlenecks, federal initiatives like the Dairy Entrepreneurship Development Scheme (DEDS) are systematically subsidizing the widespread deployment of bulk milk coolers and automated chilling centers. This top-down policy shift fundamentally guarantees the hygienic, scalable procurement necessary to support the national explosion of short-shelf-life, premium organic dairy portfolios.

Why Invest in the Dairy Industry In India: Key Growth Drivers & ROI

- Massive Consumption Base: A deeply ingrained cultural reliance on dairy, combined with a population exceeding 1.5 billion and per-capita milk availability growing at 3.1% annually, guarantees a highly resilient, high-volume consumer base. This ensures sustainable, long-term operational profitability for commercial FMCG dairy enterprises.

- Policy Support & Subsidies: Robust structural backing via state-level incentives and the National Dairy Plan actively de-risks initial capital expenditure. Investors can heavily leverage government subsidies to rapidly scale localized chilling infrastructure and advanced cold-chain logistics networks, yielding highly predictable ROI with favorable unit economics.

- Premiumization & Tech Upgrades: A lucrative shift toward high-margin value-added products is accelerating rapidly. Investments in automated milking systems and IoT-enabled farm monitoring ensure the hygienic, scalable production of premium A2 milk and organic dairy, directly expanding B2B operational margins across affluent urban demographics.

- Supply Chain Efficiencies: The explosive proliferation of quick-commerce digital platforms drastically enhances distribution efficiencies. By integrating predictive AI for demand forecasting and expanding last-mile refrigerated fleets, brands bypass legacy bottlenecks, slash perishability rates, and unlock high-velocity, near-instant access to highly lucrative Tier-2 municipal markets.

Dairy Industry In India Market Trends & Future Outlook:

- Surge in the A2 and Organic Premium Matrix: Driven by stringent clean-label sourcing demands and scientifically perceived digestive health benefits, affluent urban consumers are aggressively migrating toward premium A2 cow milk and certified organic dairy variants. Innovative industry startups are successfully commanding highly lucrative premium pricing models by adopting eco-friendly glass packaging and deploying highly sticky, direct-to-home subscription fulfillment formats, completely redefining the traditional B2C value proposition.

- Quick-Commerce Reshaping Perishable Distribution: The rapid emergence of 10-to-15-minute quick-commerce delivery platforms, such as Zepto and Blinkit, is fundamentally altering the complex shelf-life economics of the dairy sector. This advanced, hyper-local distribution network allows both massive cooperative federations and nimble private CPG brands to confidently introduce short-shelf-life, high-margin specialty desserts, flavored yogurts, and functional probiotic beverages to metropolitan markets with virtually near-zero inventory spoilage risk.

- AI and IoT-Driven Procurement Networks: Large-scale commercial processors are deeply integrating artificial intelligence and machine learning algorithms into their foundational supply chains. Real-time data analytics and automated IoT farm sensors are now considered absolutely essential operational investments for proactively predicting lean-season fodder shortages, optimizing herd health monitoring, and ensuring stringent, uncompromised quality control across tens of thousands of fragmented, village-level raw milk collection centers.

- Consolidation of Value-Added Processing: As evolving domestic consumer palettes expand significantly beyond traditional commodities like ghee and paneer, the broader market is poised to witness aggressive merger and acquisition activity alongside massive greenfield capacity expansions. Long-term corporate capital will heavily target dedicated, state-of-the-art facilities capable of manufacturing complex, globally competitive product lines, encompassing UHT milk, specialized Greek yogurt, and whey-fortified functional protein beverages.

- Blockchain Integration for Supply Chain Traceability: Responding to heightened consumer awareness regarding systemic food safety and adulteration risks, enterprise-level dairies are aggressively piloting blockchain technology to guarantee absolute end-to-end supply chain transparency. This immutable digital ledger provides sophisticated B2B buyers and retail consumers with complete visibility into the product lifecycle tracking everything from specific veterinary inputs at the primary farm level to the precise thermal parameters maintained during final retail distribution.

➤ Request Full Brochure - Discover the Complete TOC and Data Coverage

By the IMARC Group, the Top Competitive Landscape & their Positioning:

- GCMMF

- Mother Dairy Fruits & Vegetables Pvt. Limited

- Nestlé S.A. (India)

- Parag Milk Foods Ltd.

- Heritage Foods Ltd.

- Hatsun Agro Product Ltd.

- Karnataka Co-operative Milk Producers Federation Ltd.

- Tirumala Milk Products Pvt. Ltd.

- COMFED Bihar Sudha

- Prabhat Dairy (Sunfresh Agro Industries Pvt. Ltd.)

Covering an in-depth analysis of the competitive landscape, market structure, key player positioning, competitive dashboards, top winning strategies, and detailed profiles of all major industry participants you will gain access to all these exclusive insights within the full research report.

Market Segmentation Breakdown:

Analysis by Product Type:

- Liquid Milk (Dominant segment; essential staple)

- A2 Milk (Fastest growing niche)

- UHT Milk

- Organic Milk

- Flavored Milk & Yoghurts

- Cheese & Butter

- Ghee (Traditional staple with high value)

- Ice Cream

- Dairy Sweets

- Others (Paneer, Khoya, Skimmed Milk Powder)

Liquid milk dominates the India dairy product market with an overwhelming 65.30% share in 2025

Regional Insights:

- Uttar Pradesh: The largest market, supported by a vast network of cooperatives and high buffalo population.

- Rajasthan & Gujarat: Key milk-surplus states with strong cooperative structures (e.g., Amul in Gujarat).

- Delhi-NCR: Rapidly growing urban market driving demand for premium and packaged dairy.

- Maharashtra

- Karnataka

- Tamil Nadu

- Others

Uttar Pradesh anchors the dairy industry in India with the largest single-state share of 18.70% in 2025.

Recent News & Developments

- A2 Milk Expansion: Parag Milk Foods is scaling premium A2 milk and organic dairy portfolios targeting urban consumers.

- Cooperative Strengthening: National Dairy Development Board continues to modernize village-level procurement and cold-chain infrastructure.

- Global FMCG Push: Nestlé India is expanding its dairy-based nutrition and value-added product offerings.

- Private Sector Capacity Expansion: Hatsun Agro Product is investing in new processing plants to boost cheese and ice cream production.

- Amul Market Leadership: GCMMF continues to dominate through extensive cooperative networks and aggressive product diversification.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Request Customization - Align the Report Insights with Your Strategic Goals

Frequently Asked Questions (FAQs):

Q1. What is transforming the traditional dairy industry into a high-growth FMCG sector?

The shift toward value-added products like probiotics, flavored milk, and organic dairy is converting the industry from a commodity-based model into a high-margin FMCG ecosystem.

Q2. Why is A2 and organic milk gaining strong traction in India?

Health-conscious urban consumers are increasingly preferring A2 and organic variants due to perceived digestive benefits, clean-label sourcing, and premium quality assurance.

Q3. How are cooperatives shaping the Indian dairy ecosystem?

Organizations like Gujarat Cooperative Milk Marketing Federation have built scalable procurement networks, ensuring stable farmer incomes and consistent raw milk supply.

Q4. What role does technology play in modern dairy supply chains?

AI, IoT-based herd monitoring, and blockchain traceability are enhancing quality control, reducing spoilage, and improving supply chain transparency across fragmented rural networks.

Q5. Which regions dominate milk production and consumption in India?

Uttar Pradesh leads production due to its large livestock base, while urban hubs like Delhi NCR are driving demand for premium dairy products.

Strategic Insight & Verdict

From a strategic perspective, the India dairy industry is rapidly transitioning into a high-value, technology-integrated FMCG powerhouse, where leading players such as GCMMF, Mother Dairy, and Nestlé India are aggressively expanding value-added portfolios to capture premium urban demand. Simultaneously, companies like Parag Milk Foods and Hatsun Agro Product are investing in advanced processing and cold-chain infrastructure to scale high-margin categories such as cheese, whey protein, and A2 milk. Backed by strong policy support from National Dairy Development Board and increasing digital supply chain integration, the sector is evolving toward a more organized, traceable, and export-oriented ecosystem. Investors focusing on premiumization, value-added processing, and tech-enabled procurement networks are best positioned to unlock sustained, high-growth returns in this structurally expanding market.

Tarang, Digital Insights Specialist at IMARC Group: https://www.linkedin.com/in/tarang-chauhan-31a82b265/

Verified Data Source: IMARC Group

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-202071-6302